The decision by the United Arab Emirates to exit OPEC lands hardest in India, where oil prices feed directly into inflation, fiscal stability and growth.

And it could radically redraw India’s energy calculus.

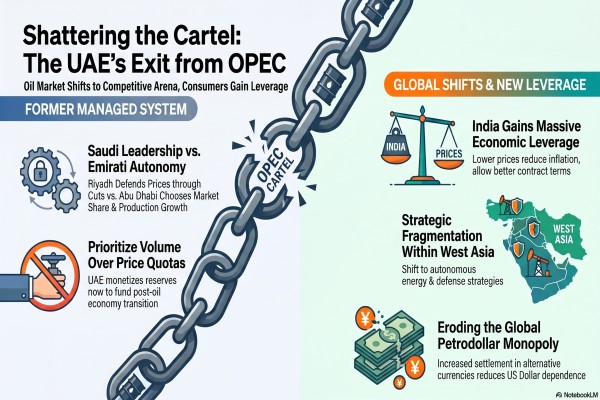

Let’s start with the core variable: price. The UAE wants to maximise output, free from OPEC quotas, to monetise reserves while demand still holds. More supply, especially from a low-cost producer, lowers the ceiling on prices over time.

For India, that means a smaller import bill and reduced inflation pressure. It also widens negotiating space. A weaker cartel cannot enforce discipline as effectively, giving large buyers like India more leverage in contracts and pricing.

Geography amplifies the gain. The UAE is a proximate supplier with deepening economic ties. Incremental Emirati barrels can flow to India faster and cheaper than from distant sources. That matters in a market where logistics and politics increasingly shape availability. If Abu Dhabi ramps up production, India can lock in volumes quickly, improving supply resilience.

The constraint is not production but transit.

Tensions involving Iran and instability around the Strait of Hormuz keep risk premiums elevated. More oil on paper does not guarantee delivery.

For India, this creates a split horizon. Medium-term price relief, short-term volatility. The policy response is clear: diversify suppliers, expand strategic reserves, and hedge routes.

The second-order effect is bargaining power. As OPEC weakens, price formation shifts from coordinated cuts to competitive output. That reduces the cartel’s ability to engineer scarcity.

India benefits from a market where producers compete for share. It can extract better terms, diversify contracts, and avoid overdependence on any single bloc.

From India, let’s widen the lens to West Asia.

The UAE’s exit exposes a widening gap with Saudi Arabia. Riyadh has long acted as the system’s stabiliser, cutting output to defend prices.

Abu Dhabi is choosing volume over price. If Saudi Arabia responds by defending market share, the outcome is a supply surge and lower prices. If it continues to cut alone, it cedes influence. Either way, cartel cohesion erodes.

That erosion matters because OPEC’s power rested on spare capacity and coordination. The UAE brings both. Its departure removes a meaningful share of flexible supply from coordinated control. The cartel’s ability to act as a shock absorber weakens. Markets become more reactive to geopolitical events and less anchored by policy signals from Vienna.

Security is the hidden driver. OPEC membership constrains unilateral responses in a region where threats are immediate.

With Iran inside the same organisation, consensus becomes friction. The UAE’s exit signals a shift towards autonomy in both energy and defence. Export security now ranks above price management. That reorders priorities across the Gulf.

The regional implication is fragmentation. Gulf states are no longer moving in lockstep. National strategies override bloc discipline. That complicates crisis management and reduces the likelihood of coordinated responses to disruptions.

It also opens space for new alignments, issue-based and transactional rather than institutional.

For the United States, the trade-off is stark.

A weaker OPEC aligns with lower prices and reduced cartel power. But the monetary angle cuts another way. If Gulf producers diversify away from dollar settlement, the foundation of the petrodollar system weakens. The UAE has signalled willingness to consider alternatives under dollar liquidity stress. That turns energy policy into financial statecraft.

Enter China. China gains from softer prices, like India, but its strategic upside is larger. Any shift towards yuan settlement in oil trade advances currency internationalisation in a sector long dominated by the dollar. Even partial adoption matters. It builds parallel rails for trade and finance, reducing exposure to dollar cycles and sanctions risk.

The constraint for China mirrors India’s. Supply security is tied to sea lanes. Disruptions in Hormuz blunt the benefit of higher output. That pushes Beijing to prioritise route security and deepen its presence in regional logistics and infrastructure. Energy policy bleeds into maritime strategy.

And then, price dynamics split across time.

In the near term, volatility persists. Geopolitical risk keeps a floor under prices even as expectations of higher UAE output cap the upside.

In the medium term, the direction is down. More unconstrained supply, weaker coordination, and competitive behaviour lower the structural price ceiling. The risk tail is a price war if major producers chase share simultaneously.

For India, the net effect is positive with caveats. Lower average prices ease macro pressures. Greater supplier competition improves terms. But volatility demands buffers. Strategic reserves, diversified sourcing, and flexible contracts become more valuable than ever.

For West Asia, the shift accelerates a move from cartel discipline to state-centric strategy. Alliances loosen. Energy policy aligns with security imperatives. The region becomes less predictable, more transactional.

For China, the opening is financial as much as energy. If even a slice of Gulf crude trades in yuan, the global system inches towards currency pluralism. That does not dethrone the dollar, but it erodes its monopoly in a critical market.

The UAE is making a clear bet: Maximise output now, convert reserves into capital, and deploy that capital into a post-oil economy. In doing so, it accepts lower prices and higher volatility in exchange for autonomy. It also signals that coordination is no longer the optimal strategy for producers with low costs and high capacity.

The consequence is an oil market that looks less like a managed system and more like a competitive arena. Prices will be set by output races and geopolitical shocks, not by quota discipline. Consumers gain leverage. Producers lose collective control. Financial flows become less dollar-centric at the margins.

India stands to gain the most in economic terms, provided it manages the security risks.

China stands to gain strategically if currency shifts follow. The Gulf enters a phase where power is dispersed and alignment is fluid.

OPEC does not disappear, but its ability to act as the central bank of oil is diminished.

The UAE has moved first. Others will decide whether to follow or resist.

Either way, the balance of energy power has already begun to shift.